At the end of 2025, we noted humility in the ability to predict outcomes but confidence in the resilience of the various portfolios we share with you, our Partners. The beginning of 2026 has strengthened our belief in those statements.

At the end of every year, firms on Wall Street produce a series of predictions for the coming year. They project a strong sense of confidence in specific price targets for the S&P 500 (amongst other indices). It is an annual rite, producing many well-researched pages of text and charts.

We read many of these publications as they often contain interesting data points that enhance our ever-changing mosaic of the world. Yet none of those firms predicted the two most compelling events for financial markets in Q1:

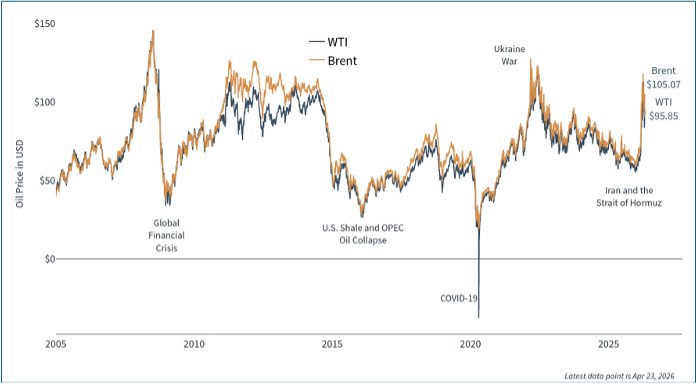

- The Iran War (launched in February), which has created massive movements in global oil prices amongst significant human strife.

- The “SaaS-Apocalypse” representing significant selloffs in software-as-a-service (SaaS) businesses whose cash flows were considered rock solid before AI began their advancements in coding that could disrupt a large swath of SaaS businesses.

WMK follows the ethos of the exemplary author and definitive scholar on randomness, Nassim Taleb, who wrote: “You can’t predict in general, but you can predict that those who rely on predictions are taking more risks…Someone who predicts will be fragile to prediction errors. An overconfident pilot will eventually crash the plane. And numerical predictions lead people to take more risks.”

We also did not have a preconceived notion that the Iran War or SaaS-Apocalypse would occur – but our portfolios are not built for singular outcomes (i.e. market stability). Rather, our process seeks to avoid unnecessary risks and own businesses that can thrive in many economic environments.

Strategic Equities

Our direct Strategic Equity portfolio owns a concentrated, yet diversified group of businesses anchored by strong cash flows, long-term competitive advantages, and run by excellent management teams. We view these as businesses, not opportunities to “trade stocks.” The composite of these portfolios was relatively more resilient than the broader stock market, declining 1.3% in Q1 vs. a 2.2% decline for the ACWI and 4.6% decline for the S&P 500.

Return on equity is a basic but reasonable measure of business quality. Our Strategic Equity portfolio generates a weighted average of ~19% ROE, compared with ~15.7% ROE for the ACWI.

Canadian Natural Resources (CNQ), which we have owned since the COVID-19 oil lows, returned 47.3% in Q1. While not a tactical bet, CNQ represents the types of competitive advantages we look for in a business, with substantial, long-life oil reserves that are fundamentally lower cost to produce than those found in other major producers in the U.S. and beyond. The stock’s move was primarily driven by the rapid rise in global oil prices driven by the Iran War impacting the Strait of Hormuz, a global chokepoint for oil movement.

The beauty of CNQ’s business model is not that they would thrive when oil prices rise (that is an accepted truth for oil & gas companies). Instead, it is that they generated strong cash flow even when oil prices are low. We are not seeking the greatest leverage to high oil prices – that would require a far more levered balance sheet – but are rather seeking a company with the greatest sustainability of earnings over time. To this end, we remain quite happy owning CNQ’s long-term cash flow generation.

Conversely, The Charles Schwab Corporation (SCHW) is a significant holding that detracted from performance in Q1, falling 5.6%. The market is concerned that Schwab’s net-interest-margin (NIM) – the yield Schwab earns on customer cash balances — will weaken as interest rates fall.

NIM will naturally fluctuate throughout economic cycles. Interest rates are entirely out of Schwab’s control. What is within Schwab’s control is growing their scale in a business model that rewards size over time. A very basic, but important, metric to monitor for Schwab is their net new asset growth. This metric measures how much cash has been contributed to new or existing accounts.

In Q1, Schwab generated a record $158 billion in net new assets. Robinhood, the brokerage firm catering to new investors (some might call them gamblers) generated $17.7 billion in net new assets over the same period. For a comparison of scale, Schwab custodies $11.8 trillion in assets vs. Robinhood’s $307 billion.

Schwab is the gold standard for being the low cost, high value provider in the brokerage space. WMK custodies most of our publicly traded assets at Schwab, so we eat our own cooking. As Schwab continues to scale, so will their ability to drive value to customers (they were the first to offer no fee trades), which is a perpetuating flywheel of scale. This virtuous cycle is not dissimilar to Amazon, which consistently finds ways to take scale and reinvest into the customer experience. We hope to benefit from this scale for years to come (and we are happy Amazon shareholders as well).

Schwab trades at ~14.8x P/E ratio vs. Robinhood at ~41x P/E ratio. We think Schwab is a better deal.

Required Reserves

Many of WMK’s Partners – including our Founder – own reinsurance entities that carry a benchmark of 90% investment grade fixed income (AGG) and 10% S&P 500 (SPY). WMK invests this portfolio with the same mental construct of avoiding unnecessary risks and creating structural resilience as in our equity portfolio.

Investment grade fixed income is a challenging space today with corporate bonds trading near historic low spreads to Treasuries. Investors receive a ~80bps premium to take on corporate credit risk vs. that of the U.S. Government. While we make no claim that the U.S. Government is “fiscally responsible” with their levels of spend (regardless of political tilt), we also recognize that the U.S. Treasury can print money to pay their bills whereas corporations cannot. Therefore, we would prefer more spread to take corporate risk.

Conversely, mortgage-backed securities trade at a 125bp spread to Treasuries. Agency MBS carry the same credit risk as Treasuries as they are guaranteed by the U.S. Government. MBS are trading at a wider spread to their historic norm of 110bps as investors are concerned about prepayment risk (i.e. homeowners refinancing as interest rates fall). WMK is less concerned about this risk. We will happily reinvest elsewhere if this risk comes to pass as we are running a lower duration portfolio than the benchmark might imply to dampen volatility in our reinsurance linked portfolios.

Our Required Reserves portfolios are positioned accordingly: overweight MBS and underweight Corporates.

Closing Thoughts

Charlie Munger once observed: “The big money is not in the buying or the selling, but in the waiting.” We promise no ability to predict the future — only positions built to withstand volatility so our Partners (and we) can wait patiently. We look forward to growing together.

Disclosures

The views expressed above are those of WMK Investment Partners. These views are subject to change at any time based on market and other conditions, and WMK disclaims any responsibility to update such views.

Past performance is not indicative of future performance. Principal value and investment return will fluctuate. There are no implied guarantees or assurances that the target returns will be achieved, or objectives will be met. Future returns may differ significantly from past returns due to many different factors. Investments involve risk and the possibility of loss of principal. The values and performance numbers represented in this report do not reflect management fees.

WMK may discuss and display, charts, graphs, formulas which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and should not be used on their own to make investment decisions. To the extent that certain of the information contained herein has been obtained from third-party sources, such sources will be cited, and are believed to be reliable, but WMK has not independently verified the accuracy of such information.